Y’all.

I am pretty excited about this update because we are finally down to only FOUR DIGITS of debt!!!!

FOUR.

Do you realize how close that makes us? That feels like almost nothing after we started with $82,000 in the hole. And after our April and May, I wasn’t even sure if we’d get to this point by the end of the year. Our goal is so near and we still have almost four months left.

This month moved the needle more than any other month. Just in August alone we were able to pay off $6,289. I can’t believe that was even possible. That’s more than double a typical month for us. Click here to see our progress.

Here’s what we did in August:

- I had an unexpectedly awesome month with my Bondbons business.

- My husband worked his tail off painting. He was given an awesome opportunity to paint apartments for three weeks. He was seriously gone for about 12-14 hours a day, but it obviously paid off.

- I did some curriculum work for my school district {always a super fun way to end the summer}

- Our water and gas bill were lower than expected—the extra money was put toward debt.

- We have money allotted to go into our emergency fund every month should we have to dip into it, but we haven’t had to for about three months. I was going to leave it in there to help cover next summer’s expenses, but decided to go ahead and pull it out and throw it at the debt. We can save up that money after our balance is $0.

I’ll close with this:

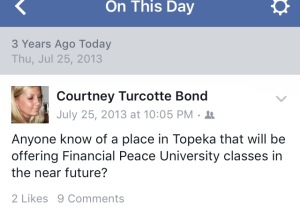

You know those memories that pop up on Facebook? I came across this post {which was actually from July . . . but we’ll apply it to August, okay?}.

I remember that night of July 25th, 2013. My husband and I had one of the biggest fights over money in our marriage. We were desperate. I put this question out there as a plea for help, and thanks to the comments I was made aware that our own church was hosting classes for FPU.

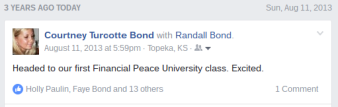

Just a few weeks later, I posted this in August:

Three years later, we have paid off over $72,000 simply by living below our means, budgeting, and putting in extra work. CRAZY. I had no idea we would be this close to being done so quickly {I was thinking it would take us six-ten years minimum at first}.

I’m so glad we made the decision to take those classes together three years ago.

Looking forward to posting about September.

Love,

![]()

record-breaking profits from September – December

record-breaking profits from September – December